Home / Income Tax Returns for AY 2020-21: Ready Reference

Income Tax Returns for AY 2020-21: Ready Referencer

With the extended time limit for filing of Income Tax Return (for AY 2020-21), u/s. 139(1), without late fees, for Non-Audit cases and for Non-Corporate assessees of 31st December 2020 fast approaching, given below is a quick guide for ready reference of some key changes that have been made in the respective Income tax return forms for this year.

Further, the conditions and features for eligibility of forms that are applicable for filing the correct income tax returns are also specified as follows:

Key Procedural Changes:

- ITR 1 to ITR 4 can be filed using PAN or Aadhar by Individuals.

- The submitted ITR forms display the ITR-V with a watermark ‘Not Verified’ until the same is verified either electronically by EVC or by sending the same via post after manual signing.

- The unverified form ITR-V will not contain any income, deduction and tax details. The unverified form will only contain basic information, E-filing Acknowledgement Number and Verification part.

- The unverified acknowledgement is titled as ‘INDIAN INCOME TAX RETURN VERIFICATION FORM’ & final ITR-V is titled as ‘INDIAN INCOME TAX RETURN ACKNOWLEDGEMENT’.

- Return filed in response to notice u/s. 139(9), 142(1), 148, 153A, and 153C must have DIN.

- There is a separate disclosure for Bank accounts in case of Non-Residents who are claiming income tax refund and not having a bank account in India.

COVID related Changes:

- The Government had extended the time limit for claiming tax deduction u/CH VIA to 31st July 2020, and the details of the same need to be reported in Schedule DI (details of Investment).

- The time limit for investing the proceeds or capital gains in other eligible assets, so as to claim exemptions u/s 54/ 54B/ 54F/ 54EC, had been extended to 30th September 2020.

- Penal interest u/s. 234A @ 1% p.m., where the payments were due between 20-03-20 to 29-06-20 and such amounts were paid on or before 30-06-20, had been reduced to 75%, vide ordinance dated 31-03-20.

- Period of forceful stay in India, beginning from quarantine date or 22-03-20 in any other case up to 31-03-20, is to be excluded, for the purpose of determining residential status in India.[1]

Consequences of Late filing of Return of Income:

- Late Fees u/s. 234F of INR. 5,000 up to 31.12.20 and INR. 10,000 up to 31.03.21. In case of total income up to 5 Lacs, the penalty is INR. 1,000.

- Penal Interest u/s. 234A @ 1% per month

- Reduced to 75%. vide Ordinance dated 31.03.20, where the payments were due between 20.03.20 to 29.06.20, and such amounts were paid on or before 30.06.20.

- Vide CBDT Notification dt 24.06.2020, no interest u/s 234A if Self-Assessment tax liability is less than 1 Lac and the same has been paid before the original due date.

- In case of a belated return, loss under any head of Income (except unabsorbed depreciation) cannot be carried forwarded.

- Deduction claims u/s. 10A, 10B, 80-IA, 80-IB, etc would not be allowed.

Consequences of Late filing of Return of Income:

- Late Fees u/s. 234F of INR. 5,000 up to 31.12.20 and INR. 10,000 up to 31.03.21. In case of total income up to 5 Lacs, the penalty is INR. 1,000.

- Penal Interest u/s. 234A @ 1% per month

- Reduced to 75%. vide Ordinance dated 31.03.20, where the payments were due between 20.03.20 to 29.06.20, and such amounts were paid on or before 30.06.20.

- Vide CBDT Notification dt 24.06.2020, no interest u/s 234A if Self-Assessment tax liability is less than 1 Lac and the same has been paid before the original due date.

- In case of a belated return, loss under any head of Income (except unabsorbed depreciation) cannot be carried forwarded.

- Deduction claims u/s. 10A, 10B, 80-IA, 80-IB, etc would not be allowed.

Vide CBDT Notification dt 24.06.2020, no interest u/s 234A if Self-Assessment tax liability is less than 1 Lac and the same has been paid before the original due date.

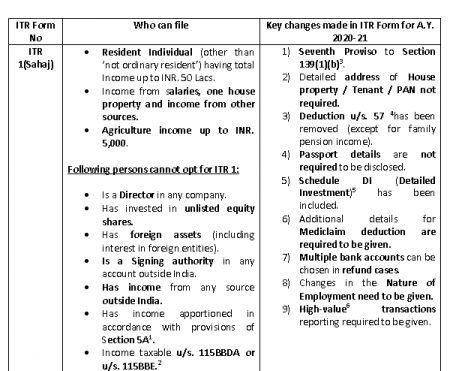

- Section 5A: Apportionment of income between spouses governed by the Portuguese Civil Code.

- 115BBDA: Tax on dividend from companies exceeding Rs. 10 Lakhs; 115BBE: Tax on unexplained credits, investment, money, etc. u/s. 68 or 69 or 69A or 69B or 69C or 69D.

- Inserted in sec 139(1) by Act No. 23 of 2019, w.e.f. 1-4-2020:

Provided also that a person referred to in clause (b), who is not required to furnish a return under this sub-section, and who during the previous year:

- has deposited an amount or aggregate of the amounts exceeding one crore rupees in one or more current accounts maintained with a banking company or a co-operative bank; or

- has incurred expenditure of an amount or aggregate of the amounts exceeding two lakh rupees for himself or any other person for travel to a foreign country; or

- has incurred expenditure of an amount or aggregate of the amounts exceeding one lakh rupees towards consumption of electricity; or

- fulfils such other conditions as may be prescribed,

Shall furnish a return of his income on or before the due date in such form and verified in such manner and setting forth such other particulars, as may be prescribed.

4. Section 57: Deduction against income chargeable under the head “Income from other sources”.

5. Schedule DI: Investment eligible for deduction against income (Ch VIA deductions) to be bifurcated between paid in F.Y.19-20 and during the period 01-04-20 to 31-07-20.

6.High-value Transaction: Annual Cash deposit exceeding Rs. 1 crore or Foreign travel expenditure exceeding Rs. 2 Lakhs, Annual electricity expenditure exceeding Rs. 1 Lakh.

7.Schedule 112A: From the sale of equity share in a company or unit of equity- oriented fund or unit of a business trust on which STT is paid under Section 112A.

8. 115AD(1)(iii) proviso: for Non-Residents – from the sale of equity share in a company or unit of equity-oriented fund or unit of a business trust on which STT is paid under Section 112A.

9. Section 40(ba): any payment of interest, salary, bonus, commission or remuneration paid to a member in case of Association of Person (AOP) or Body of Individual (BOI).

10. Section 90 & 90A: Foreign tax credit in cases where there is a bilateral agreement; Section 91: Foreign tax credit in cases of no agreement between the countries.

[1] Circular No 11 of 2020 dated 08th May 2020.

References

Image Credits: Photo by Markus Winkler from Pexels

Related Posts

India’s Tax Framework from 1 April 2026: Key Changes, Proposals and Practical Implications

Enterprise Value Enters the Picture: IBBI’s Valuation Reforms

India’s Legal Vulnerability in Light of Strait of Hormuz Closure